When people compare insurance, trauma insurance and health insurance often get lumped into the same mental box. They both talk about illness. They both show up when things go wrong. And they both sound like they’re meant to “help”.

But they solve very different problems.

If you’re weighing up whether you need trauma insurance, health insurance, or both, the real question isn’t which one is better. It’s what kind of financial pressure you’re trying to protect yourself from.

The short answer: Yes, having both trauma insurance and health insurance can absolutely help, because they cover different parts of the same crisis. Let’s break it down properly.

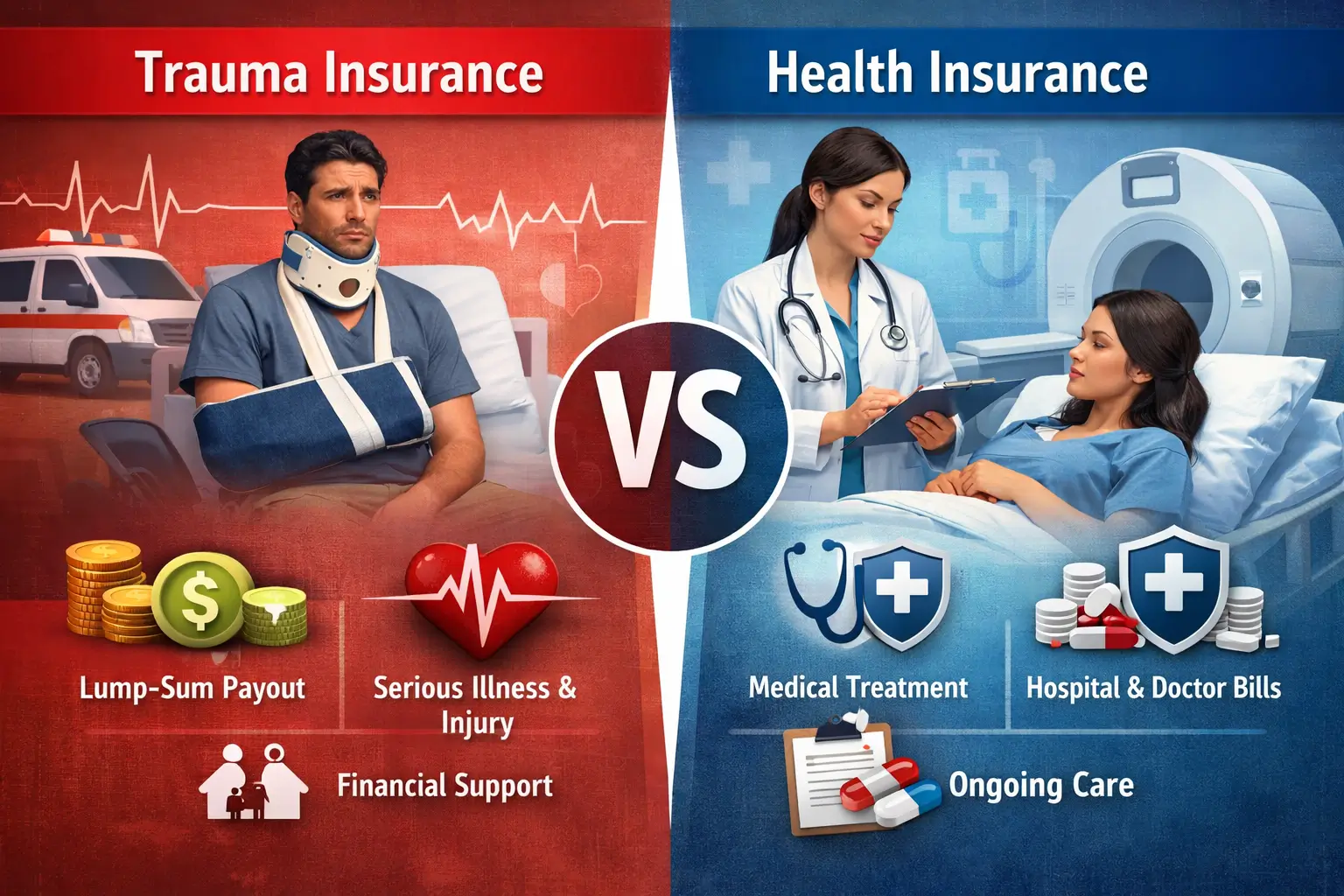

What health insurance actually does

Health insurance in New Zealand is designed to help cover medical treatment costs. Depending on your policy, it may help pay for:

- Private hospital treatment

- Specialist consultations

- Diagnostic tests and scans

- Some elective procedures

Health insurance is mostly about access and speed. It can help you:

- Get treatment sooner

- Choose private care where available

- Reduce out-of-pocket medical costs

What it generally does not do is replace income, pay your mortgage, or cover everyday living expenses while you’re unwell. Health insurance looks after the treatment. Not the ripple effects.

What trauma insurance actually does

Trauma insurance (also called critical illness insurance) pays a lump sum if you’re diagnosed with a serious, policy-defined illness or injury.

That payout is not tied to receipts or treatment invoices. You can use it however you need. Trauma insurance is about financial flexibility during a health crisis. It can help with:

- Time off work (for you or your partner)

- Mortgage or rent repayments

- Household bills

- Childcare or home help

- Recovery, rehab, or lifestyle adjustments

- Taking pressure off while you focus on getting better

If health insurance pays the surgeon, trauma insurance pays for life to keep moving.

Why health insurance alone often isn’t enough

A common assumption is: “If I’ve got health insurance, I’m covered.” That’s only partially true. Health insurance may help with:

- The operation

- The hospital stay

- The specialist

But it usually won’t help with:

- Lost income

- Ongoing living costs

- Your partner needs time off work

- Childcare disruptions

- Mortgage pressure

- Emotional breathing room

A serious illness doesn’t just create medical costs; it disrupts cash flow. That’s where trauma insurance steps in.

Why trauma insurance alone also has limits

Trauma insurance NZ gives you money, but it doesn’t guarantee access to treatment. Without health insurance:

- You may rely solely on the public system

- Waiting times can vary

- Some private options may still be out of reach or delayed

Trauma insurance gives you options, but health insurance can improve speed and choice when it comes to care. Together, they cover both sides of the problem.

How trauma insurance and health insurance work together

Think of it like this:

Health insurance helps manage medical access and costs. Trauma insurance helps manage life disruption and financial stress. When used together, health insurance helps you get treated, while trauma insurance helps you stay financially stable

- You’re not forced back to work too early

- You’re not draining savings or selling assets

- You’re not making recovery decisions based on money panic

It’s not about doubling up. It’s about layering protection.

A real-world example

Imagine you’re diagnosed with cancer. With health insurance only:

- Treatment costs may be covered

- You may still lose income during recovery

- Your partner may need unpaid leave

- Mortgage and bills still exist

- Savings start draining fast

With trauma insurance only:

- You receive a lump sum

- You still rely on public treatment timelines

- You may use the payout to bridge gaps, but access may be slower

With both:

- Health insurance supports treatment and speeds

- Trauma insurance supports income, family, and lifestyle stability

- You recover without financial freefall

That’s the difference.

Do you need both trauma and health insurance?

Having both is especially helpful if you:

- Rely on your income to meet financial commitments

- Have a mortgage or dependants

- Are you self-employed or contract-based

- Have limited emergency savings

- Want flexibility during recovery

- Don’t want medical or financial decisions dictated by pressure

It’s less about age and more about exposure. How many things fall apart if you can’t function normally for a while?

Where ACC fits (and where it doesn’t)

ACC plays an important role in New Zealand, but it mainly covers accidental injuries, not illnesses. Conditions like cancer, stroke, or degenerative diseases usually aren’t ACC claims.

That’s why trauma insurance is often considered alongside health insurance; it helps cover gaps that ACC doesn’t.

Common misconceptions

“Health insurance replaces trauma insurance.”

It doesn’t. One pays for treatment. The other pays for life.

“Trauma insurance is only for older people.”

Serious illness doesn’t wait for retirement.

“I’ll just use savings if something happens.”

Many people underestimate how quickly savings disappear during long recoveries.

How an adviser helps structure both

An experienced insurance adviser can help:

- Compare NZ health insurance policies properly

- Structure trauma insurance alongside life and income protection

- Avoid overlapping or unnecessary cover

- Plan for affordability and future flexibility

So, does it help to have both?

Yes, because they protect different pressures created by the same event. Health insurance helps you get treated. Trauma insurance helps you keep living.

Together, they give you time, options, and dignity when life throws something heavy your way.

If you’re unsure whether your current health or trauma insurance actually works together, we can help review your options across leading NZ insurers and explain everything in plain English. Talk to NZ Insurances today.

.jpg)

.jpg)